Jump to section

Your air conditioner just failed.

Or maybe the repair estimate is high enough that replacement is finally making more sense than continuing to patch together an aging system.

Now you're staring at numbers that might range from $14,000 to $35,000 or more and asking the same question most homeowners ask:

How am I supposed to pay for this?

Unlike a vehicle purchase, HVAC replacement isn't something most people plan years in advance. It's often an unexpected expense that shows up during the hottest week of the year, when your family needs cooling now and you don't have the luxury of spending months evaluating financial options.

The good news is that most homeowners have more options than they realize.

Whether you're considering financing through an HVAC company, using a home equity line of credit, taking advantage of a promotional credit card offer, or paying from savings, each option comes with advantages, trade-offs, and situations where it makes the most sense.

In this guide, you'll learn:

- The five most common ways homeowners pay for an HVAC replacement

- Which payment options make the most sense for different situations

- When financing is smart, and when it isn't

- How HVAC financing actually works

- What to watch for before signing a financing agreement

- How rebates and incentives may reduce your out-of-pocket cost

The 5 Most Common Ways Homeowners Pay for an HVAC Replacement

When homeowners replace a heating and cooling system, most use one of five payment strategies.

The right option depends on your financial situation, timeline, available credit, and how urgently the replacement is needed.

1. Paying Cash or Using Savings

If you have the funds available, paying for the system outright is usually the least expensive option in terms of total cost.

You avoid interest charges, loan fees, and long-term monthly obligations.

However, cash isn't automatically the best choice simply because you have it.

For many homeowners, draining an emergency fund to pay for an HVAC system creates a different financial risk. If replacing your system would leave you without adequate savings for medical expenses, vehicle repairs, or other emergencies, financing part of the project may actually be the more conservative decision.

The goal isn't simply avoiding debt.

The goal is maintaining financial stability after the installation is complete.

2. Using a Home Equity Loan or HELOC

For homeowners with substantial equity, a home equity loan or home equity line of credit (HELOC) is often one of the most cost-effective financing options available.

Because the loan is secured by your home, interest rates are often lower than unsecured financing.

A HELOC can be particularly attractive because you borrow only what you need and pay interest on that amount rather than receiving a lump sum upfront.

The trade-off is time.

Unlike HVAC financing offered at the kitchen table during an estimate appointment, home equity financing typically requires underwriting, documentation, and lender approval.

If your system still has some life left and you're planning ahead, this may be worth exploring.

If your AC failed yesterday during a Cypress summer, you may need a faster solution.

3. Using a Promotional Credit Card

For homeowners with strong credit and a clear payoff strategy, a promotional credit card can sometimes provide a short-term financing solution.

Many cards offer introductory periods with no interest for a specified number of months.

Some also offer rewards or sign-up bonuses that can provide additional value when making a large purchase.

The key word here is discipline.

A promotional offer only works if you can realistically pay the balance before the introductory period expires.

Otherwise, the interest rate that follows may significantly increase the overall cost of the purchase.

4. HVAC Company Financing

This is the option most homeowners ultimately choose.

HVAC financing is popular because it's fast, convenient, and specifically designed for large home-comfort purchases.

Approval decisions are often returned within minutes.

Monthly payments can be spread across multiple years.

Many programs offer promotional terms that help make replacement more manageable.

However, HVAC financing also tends to be the option homeowners understand the least.

The terms vary dramatically from lender to lender, which is why it's important to understand exactly what you're agreeing to before signing.

We'll cover that in detail later in this guide.

5. Rebates and Incentives

While rebates don't pay for an entire HVAC replacement, they can reduce the amount you need to finance.

Depending on the equipment being installed, homeowners may qualify for:

- Manufacturer rebates, like the Daikin FIT instant rebate running through July 31, 2026

- Utility incentives

- Energy-efficiency rebates

These programs change regularly, and eligibility depends on the equipment selected.

A qualified HVAC contractor should be able to explain what programs may apply to your installation and how they affect the final project cost.

Which HVAC Payment Option Is Best for Your Situation?

There isn't a single best financing option.

There is only the option that best fits your circumstances.

If your primary goal is paying the least overall

Cash or a low-interest home equity loan is often the most cost-effective solution.

If your primary goal is keeping monthly payments low

Longer-term HVAC financing may provide the lowest monthly obligation, although total interest paid may increase.

If your system failed unexpectedly

HVAC financing is often the fastest path from estimate to installation.

If you have strong credit and a payoff plan

A promotional credit card may help you avoid interest altogether.

If preserving cash reserves matters most

Financing part or all of the project can allow you to keep emergency funds available for future needs.

The best decision isn't always the one with the lowest interest rate.

It's the one that supports your overall financial situation while still solving the comfort problem in your home.

Before Financing Anything, Make Sure Replacement Is Actually Necessary

Before discussing loans, payments, or financing programs, it's important to verify that replacement is truly the right decision.

Financing a replacement you didn't need is far more expensive than financing a replacement you did.

A qualified technician should be able to explain:

- The age and condition of your system

- The repairs currently required

- Expected remaining lifespan

- Estimated future repair costs

- Whether replacement is financially advantageous over the next five to ten years

That conversation should provide clarity, not pressure.

If you're still evaluating whether replacement is the right move, our Repair vs. Replace guide walks through the decision-making process in greater detail.

What Does HVAC Replacement Actually Cost in Cypress and Katy?

The cost of replacement directly affects which financing option makes sense.

While every home is different, most complete system replacements in Cypress, Katy, Bridgeland, Towne Lake, and surrounding areas fall somewhere between approximately $14,000 and $22,000.

System size, efficiency level, ductwork requirements, installation complexity, and equipment selection all influence final pricing.

We've covered those variables in detail in our HVAC replacement cost guide.

Once you've determined replacement makes sense, the next question becomes how to structure payment in a way that aligns with your financial goals.

How HVAC Financing Actually Works

When an HVAC contractor offers financing, they are typically working with a third-party lender.

The contractor installs the equipment.

The lender provides the financing.

These programs typically include:

- Loan amount

- Interest rate

- Loan term

- Monthly payment

- Promotional terms

- Credit qualification requirements

At The General, we use a multi-lender platform called Optimus, which evaluates multiple lending options simultaneously and presents available offers based on your credit profile.

Regardless of the lender involved, remember that these are real loan agreements and deserve the same level of review you would give any significant financial commitment.

What Financing Looks Like for Different Cypress and Katy Homeowners

Financing isn't one-size-fits-all.

A few common examples illustrate why.

The Emergency Summer Replacement

A family in Towne Lake loses cooling in July.

The system is beyond repair.

Waiting three weeks for a bank loan isn't realistic.

HVAC financing may be the best practical solution because speed becomes part of the value.

The Long-Term Homeowner

A homeowner plans to stay in their home another fifteen years.

They have significant equity and time to evaluate options.

A HELOC may provide lower borrowing costs and greater flexibility.

The Cash-Conscious Family

A homeowner has enough savings to pay for the installation but would deplete most of their emergency fund by doing so.

Financing a portion of the project may preserve financial flexibility while still solving the comfort problem.

The best financing option depends as much on life circumstances as it does on interest rates.

What to Read Before Signing Any Financing Agreement

This is the section worth slowing down for. The terms are where a financing decision is either a good one or an expensive one, and they're easy to skim past when you just want the AC working again. A few minutes reading them now saves you from surprises later.

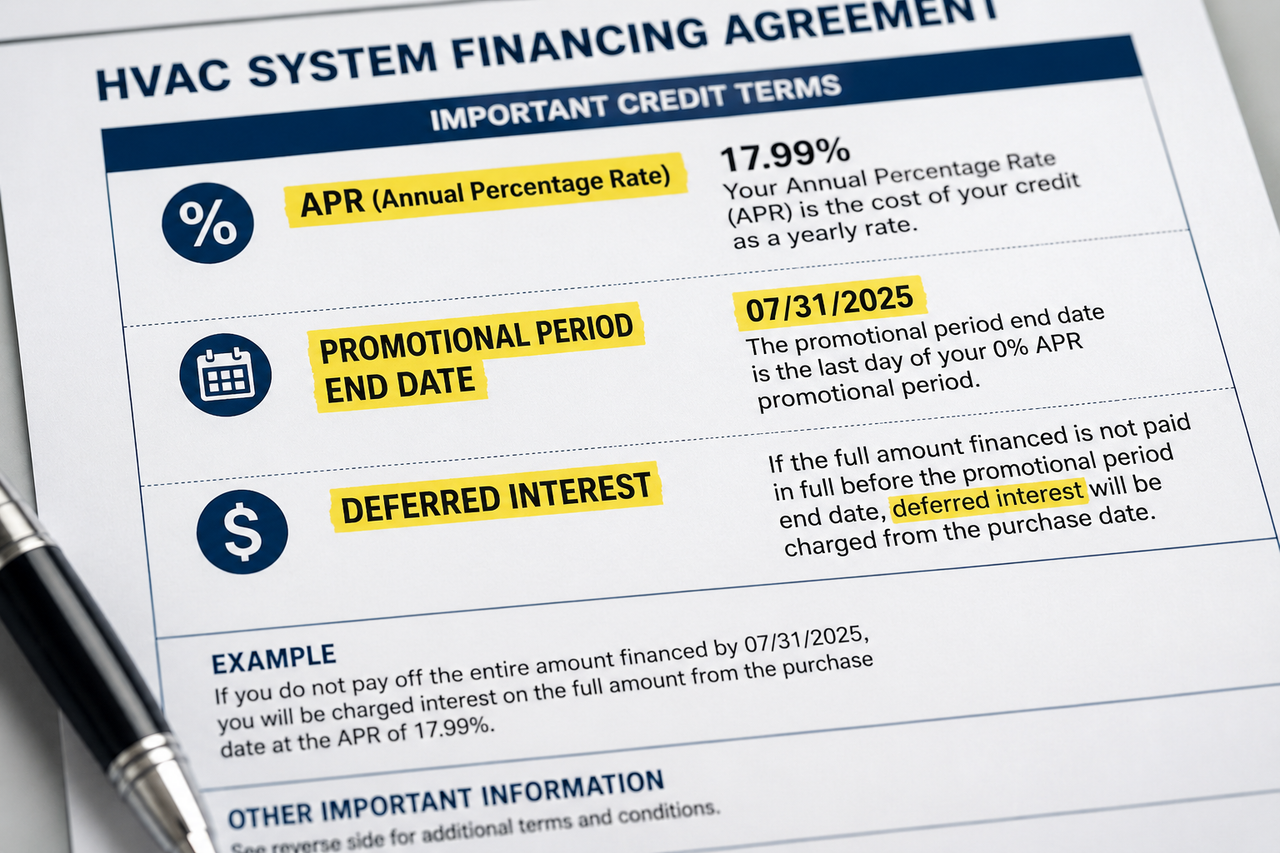

APR (Annual Percentage Rate)

This is your true cost of borrowing, expressed as an annual percentage. A 0% promotional offer sounds ideal, and it can be, but the terms around what happens after the promotional period are critical. Know the go-to rate before you sign.

Promotional period terms

Many HVAC financing offers include a "no interest if paid in full" period; often 12, 18, or 24 months. This sounds like 0% interest. It is, but only if you pay the balance in full before the period ends.

If you don't pay it in full, the interest that accrued during the promotional period is often added back to your balance retroactively.

This is called deferred interest, and it catches a significant number of borrowers off guard.

Repayment term

A longer term means lower monthly payments and more total interest paid. A shorter term means higher monthly payments and less total interest. Run the math both ways. A $12,000 system at 9.99% APR over 84 months costs meaningfully more than the same system paid off in 36 months.

Prepayment penalties

Some loans penalize you for paying off the balance early. Check for this specifically. You want the flexibility to pay it down faster if your financial situation allows.

What happens if you miss a payment. Late fees, rate changes, and credit reporting are all specified in the agreement. Read this section.

Red Flags in HVAC Financing Offers

Not every financing offer you encounter is structured to serve your interests. Here are things to watch for.

Urgency pressure. If a company is telling you that the financing rate is only available today, or that you need to sign before they leave the house to lock in the price, slow down. Legitimate financing terms don't expire at the end of the appointment.

Pressure to sign quickly is pressure to skip reading.

Verbal-only terms. Any financing offer should come with documentation you can read. If someone is telling you the terms but not showing them to you in writing, that's a problem.

Interest rate buried in the paperwork. The APR should be clearly stated. If it takes real searching to find the interest rate in the agreement, that's intentional.

Monthly payment emphasis over total cost. A company that quotes only the monthly payment ("just $189 a month!") without discussing the total cost, the term length, or the interest rate is making the financing look more attractive than it may be.

Equipment-only quotes. Make sure the financing covers a complete system with installation, not just the equipment. Some quotes separate equipment and labor in ways that aren't obvious initially.

HVAC Financing Doesn't Have to Be Complicated

Replacing an HVAC system is a major expense.

For many homeowners, the financial side of the decision feels more stressful than choosing the equipment itself.

The good news is that you have options.

Whether you use savings, home equity, a promotional credit card, rebates, or HVAC financing, the goal is the same: finding a solution that restores comfort without creating unnecessary financial strain.

Now that you understand how HVAC financing works, what questions to ask, and what warning signs to watch for, you're in a much stronger position to make a confident decision.

If you're still trying to determine whether replacement is the right move, your next step should be reading our HVAC Repair vs. Replace guide. It walks through the factors that determine when continued repairs make sense and when replacement becomes the better long-term investment.

If your system is approaching replacement age and you'd like help evaluating equipment options, installation costs, and available financing programs, our team is happy to walk you through the process and provide written estimates you can compare carefully and comfortably.

Schedule a complimentary System Replacement Estimate with The General Heating & Air.

Know the Number Before You Plan to Pay

It is easier to choose how to pay once you know roughly what you are paying for. Our HVAC replacement cost estimator gives you a price range for a new system in a couple of minutes, no phone call or email required.

Frequently Asked Questions

Does applying for HVAC financing affect my credit score?

Maybe. Many HVAC financing programs begin with a pre-qualification process that uses a soft credit inquiry, which typically does not affect your credit score. This allows homeowners to see potential financing offers before deciding whether to move forward. However, if you choose to proceed with a financing application, most lenders will perform a hard credit inquiry, which can temporarily lower your credit score by a small amount. If you're comparing multiple financing offers, it's often best to do so within a short time period. Credit scoring models generally recognize that consumers shop for financing and may treat multiple inquiries for the same type of loan as a single inquiry when made within a designated window.

What's the cheapest way to pay for an HVAC replacement?

Paying cash is usually the least expensive option because there are no interest charges or loan fees. However, the cheapest option isn't always the best option. If paying cash would significantly reduce your emergency savings, financing part of the project may provide greater financial flexibility.

Should I use my savings or finance my HVAC replacement?

This depends on your financial situation. Some homeowners prefer to avoid debt and pay upfront. Others choose financing so they can preserve cash reserves for emergencies, medical expenses, home repairs, or other unexpected costs. The right decision is usually the one that allows you to replace the system without creating financial strain elsewhere.

Is a HELOC better than HVAC financing?

Not necessarily. Home equity loans and HELOCs often offer lower interest rates, but they generally take longer to arrange and use your home as collateral. HVAC financing is typically faster and easier to obtain during the replacement process. Comparing the total borrowing cost under both options is usually the best approach.

Can rebates or incentives reduce the amount I need to finance?

Potentially. Depending on the equipment you choose and the programs available at the time of installation, rebates and utility incentives may reduce your out-of-pocket cost. These programs change periodically, so it's worth asking your contractor what incentives may apply to your project, and verifying what is available at the time you receive your estimate.

Is 0% HVAC financing actually free?

Sometimes. Many promotional offers provide no interest if the balance is paid in full before the promotional period ends. However, some programs include deferred-interest provisions that can add previously accrued interest back to the balance if the loan isn't paid off within the required timeframe. Always read the terms carefully.

Should I replace my HVAC system if I can't pay cash?

Not necessarily. If replacement is genuinely the best long-term solution, financing may allow you to avoid continuing repair costs while restoring comfort and reliability to your home. The important question isn't whether you can pay cash, it's whether the replacement makes financial sense compared to continuing to repair an aging system.

How much do most homeowners put down on a new HVAC system?

It varies by lender and financing program. Some financing options require no money down, while others may offer better terms if you make a larger upfront payment. Many homeowners choose a combination approach, using some savings to reduce the amount financed while preserving part of their emergency fund.